The affluent don’t just live better – they live longer – which is a problem for inequality.

Photo: http://bit.ly/1TZwNlc

Photo: http://bit.ly/1TZwNlc

The engine of inequality is firing on all pistons: Low-wage workers earn less while they’re working, and then get less in Social Security benefits once they retire.

Inequality rears its head in many ways in contemporary America, most obviously in income and wealth. But the growing economic divide in our society affects all aspects of our lives – including life expectancy. As a recent Oxfam report noted, “Rising economic inequality also compounds existing inequalities.”

Widening life-expectancy disparities seem to track widening income inequality, just as stagnating life expectancy parallels wage stagnation. As inequality has grown in the US over the last 35 years, the highest 10 percent of earners at age 50 have seen impressive gains in life expectancy—8.7 years for men and 6.4 years for women—while those in the bottom third are essentially living no longer than they did a generation ago, according to a new study from the Brookings Institution.

The difference persists for both women and men. A generation ago, women in the top 10 percent of earners had life expectancy 3.7 years longer than women in bottom 10 percent. By mid-2000s, that difference for women was 10.1 years. For men, a generation ago, the difference in life expectancy between the top 10 percent and bottom 10% was 4.9 years. By the mid-2000s, it was 12.0 years.

While some reasons for this growing gap are a mystery, others are intuitive: upper-income Americans have better nutrition, superior health care, more leisure opportunities, jobs that are likely to be less physically demanding and dangerous, time for self-care, and less worry about whether they must work while they have the flu to earn $9 an hour to try to pay their bills.

It’s long been known that the rich tend to be healthier than the poor, but there has never been such a wide difference as there is today in the United States. And despite the life expectancy gains for wealthy Americans, the US life expectancy gains lag behind those of Western Europe, Japan, and South Korea according to the Organization for Economic Cooperation and Development.

The Brookings report echoes recent research by Princeton economists Anne Case and Angus Deaton; but it takes the argument further by not only quantifying differences in lifespan by income but also by demonstrating that those with lower earnings and shorter lifespans receive considerably less in lifetime Social Security benefits.

In the mid-1980s, retired women of all incomes generally survived to collect benefits for roughly the same number of years, the Brookings study found. By contrast, the typical upper-income woman retiring in the mid-2000s could expect to collect benefits for six more years than a woman in the bottom 40 percent of the earnings distribution.

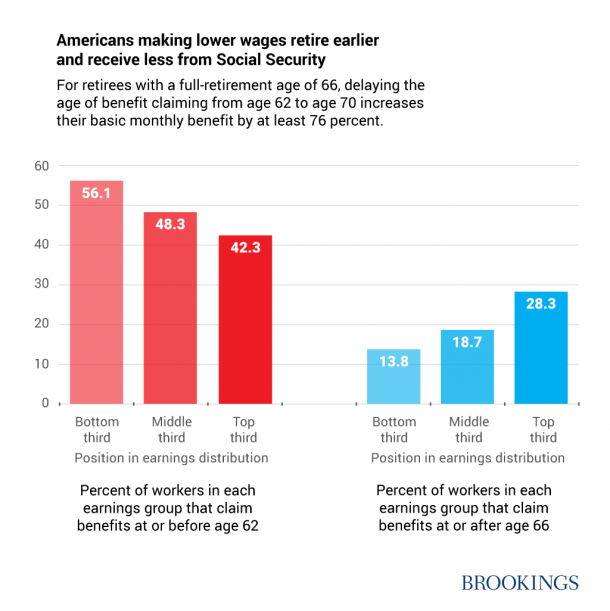

Although the income floor Social Security provides has a significant equalizing effect, lifetime benefits are a function of three things: one’s earnings while working, earnings when one retires, and how long one lives in retirement. Lower-income workers tend to retire earlier, because they tend to do more onerous, and physically demanding work, than those with high incomes. At first blush, this might seem to even out the life expectancy differential in benefits, but it actually has the opposite effect. If a worker waits to collect Social Security, at 70, he or she receives a monthly check 75 percent larger than someone who started collecting at 62 (generally a lower income worker). So high-income retirees (who tend to retire later but live longer) tend to get disproportionately more in lifetime benefits while lower-income workers generally get slammed.

This is all on top of the reality that lower-wage workers are also less likely to have private pensions or personal savings, and forego added income from working longer. Retirees at the 95th percentile in net worth had about $3 million in assets in 2013, compared to $6,400 for those at the 10th percentile, according to the Federal Reserve.

Beyond the policy implications, a bigger truth is at stake: Life does not have a price, and a long, healthy life is an existential good. Reducing inequality must address the links between economics and longevity.